One of the first investing questions people ask me is, “When is the best time to start investing?” The answer is almost always now.* If you are new to investing, keep reading to learn how to start investing, today. This is long-term index fund investing simplified.

*If you have any high-interest debt (7%+), prioritize paying that off before investing. If you don’t have an emergency fund (3-6 months of expenses in a savings account), prioritize that first.

If you don’t have any high-interest debt and you’re ready to begin long-term investing, here is how to start investing today, with 5 easy steps.

- Define your goals

- Decide on contribution amounts

- Open an investment account

- Contribute to the account

- Buy investments

Please note: I am not a licensed financial advisor. This information is for educational purposes only and is NOT financial advice. The content in this post is personal opinion based on research and math. Every individual is unique and accordingly will have varying results. Always do your own research and due diligence before making any decision.

Define your goals

Why do you want to start investing? Perhaps you want to save for retirement, build wealth, reach financial independence, or all of the above!

A goal gives you direction. The reason why you want to achieve your goal provides motivation.

At some point in your investing journey, you will encounter obstacles. Having a strong foundation, your goal and motivation, will help you preserve.

Define your goal by including what you are investing for, a timeframe, and a target amount by the end of the timeframe.

One common investing goal is investing for retirement.

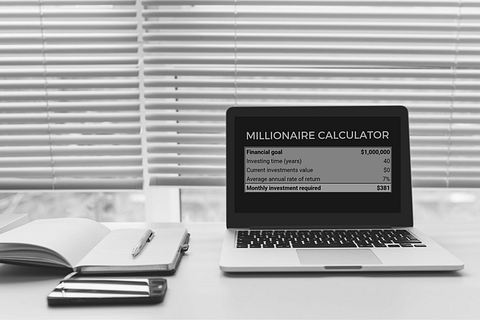

Here’s a free calculator you can use to estimate how much money you’ll need invested to retire.As an example, let’s say Blair wants to have $1 million invested within the next 20 years to reach financial independence (FI). (This goal will serve as our example in the following steps as well.)

Decide on contribution amounts

Once you have your goal, you can decide how much you’ll contribute. Your initial contribution is called your principal. Any subsequent investments are called payments or contributions.

3 Ways To Determine Contributions

There are three ways to determine your principal and payment.

1) You may already have a set amount of money you want to invest. Perhaps you have more money in a savings account than you need. Or maybe you unexpectedly got a large sum of money. (If so, good for you!!) This could be your principal.

Principal – a one-time, initial investment amount.

2) You can look at your financial plan (or budget) and see how much money you could allocate each month for investments. If you earn more than you spend, you could invest your monthly surplus. This could be your payment.

Payment – reoccurring contributions into investment accounts.

If you don’t have a financial plan, you can check out this google sheets template, the Personal Finance Planner.

3) You can calculate what your monthly payment would need to be to reach your goals.* In the example earlier (FI with $1 mil in 20 years), it would take a monthly payment of ~$2,000.

*If you want to calculate how much it would take, you can use this free calculator you can use to estimate your monthly payment.Alternatively, you could also use this free future value calculator online. The S&P 500 has returned an average of 7% over the last 100 years, and it’s used as a benchmark. That’s where the 7% average annual rate of return comes from in this example. This calculation is an estimate only.

Blair has considered these three options. Even though she would need to contribute $2,000 each month to reach her goals, her budget doesn’t have room for that right now. Instead she could comfortably invest $1,000 per month, so that’s what she will do for now.

Determine which investment accounts to prioritize

Once you’ve decided how much you are going to invest, determine which accounts are best for you.

Here’s a general order experts recommend:

- 401(k) up to employer match

- Roth IRA up to the max*

- HSA up to the max*

- 401(k) up to the max

- Brokerage

*The Roth IRA and HSA are fairly equal. Consider your own financial situation to determine what’s best for you.

All the accounts, besides the brokerage account, have contribution limits. Not all of these accounts will apply to everyone. There are also rules and restrictions on them. Visit the IRS website for the latest information on these investment accounts.

Figure out which accounts you are eligible for and prioritize accordingly.

The next step is to open the account. If it’s a 401(k) or HSA, it will likely happen through your employer. If it’s an IRA or a brokerage account, you will open it yourself.

Look into reputable low-cost brokers for IRAs and brokerage accounts. Low-cost brokers include Vanguard, Fidelity, and Charles Schwab.

Contribute to the account(s)

The next step is to make contributions. This is where you transfer the money to your account. If you have a 401(k), this is often automatically contributed from your paycheck.

If you are doing a Roth IRA or brokerage account, you will follow the instructions from your broker to transfer the money.

Some brokers will let you set up auto transfers from your bank account to your investment account. This could ensure you remember to contribute every month.

An HSA may be through an employer or you may be eligible to open it yourself.

Account Contribution Example

For our example earlier, let’s say Blair’s salary is $50,000 and her employer match will match up to 5% of her salary. That’s $2,500. Since she has $1,000 per month to contribute, here’s what her contributions may look like for the year.

| Month | Account & Amount |

| January | 401(k) $1000 |

| February | 401(k) $1000 |

| March | 401(k) $500 Roth IRA $500 |

| April | Roth IRA $1000 |

| May | Roth IRA $1000 |

| June | Roth IRA $1000 |

| July | Roth IRA $1000 |

| August | Roth IRA $1000 |

| September | Roth IRA $500 HSA $500 |

| October | HSA $1000 |

| November | HSA $1000 |

| December | HSA $1000 |

| 401(k) Total | $2,500 |

| Roth IRA Total | $6,000 |

| HSA Total | $3,500 |

| Total Invested | $12,000 |

At the time of writing (2022), the maximum 401(k) contribution is $20,500.* The maximum IRA contribution is $6,000.* The maximum HSA contribution is $3,650 for individuals and $7,300 for families.

*There are catch-up contributions for those older than 50.

Buy Investments

It’s so disheartening to hear stories of people who funded their accounts but then didn’t buy investments.

You have to purchase investments for your money to be invested! Otherwise, it’s just having cash in an investment account, which doesn’t do you any good.

Do your own due diligence and research to determine which investments to purchase. A good place to start is looking into low-cost index funds.

Learn more about the benefits of index fund investing here. (Spoiler alert: it’s an easy approach that typically outperforms 90% of investing professionals over the long term.)

Once you decide what you’ll invest in, consider setting up auto-investments. That means your money will automatically be invested into the investments you choose.

How to start investing: next steps

Now you know how to start investing. If you want a template to help you define your investing goals and track your contributions, download the Personal Finance Planner.

It will make it clear how to start investing to reach your goals. Hold yourself accountable for the goals you’ve set today.

To get daily personal finance tips, follow us on TikTok and Pinterest.

Receive weekly newsletters and exclusive freebies when you join the Wealthy Women Club. Check it out here.Would anyone else be interested in this information? Share this with them!