You’re on your investing journey and you wonder, how much should I invest? Whether you are just starting or are several years in, this is a critical question to consider. The answer will vary since everyone has unique goals and current financial landscapes.

These 4 steps will help you estimate the investment contributions required to reach your financial goals.

Please note: I am not a licensed financial advisor. Accordingly, this information is for educational purposes only and is not advice. Every individual is unique and no one’s outcomes will be exactly the same. Always do your own due diligence before making any financial decision.

Define your financial goals

The first step to answering “how much should I invest?” is setting financial goals. Now even though you’ll be setting financial goals, forget about money. Instead, picture your dream life. What does it look like?

Here are 5 prompts to help you explore what your dream life truly involves.

When you’re defining your dream life, you may realize it’s not as far out of reach as you may have thought.

In fact, as weird as it may sound, your dream life has a price. Here’s how you can calculate the cost of your dream life.

First, determine how much one year of living your dream life would cost. Now multiply it by 25.

Once you have 25 times your annual expenses invested, you are financially independent. That means your investments will support your lifestyle indefinitely.* At this point, nothing is stopping you from retiring, possibly even early.

*According to the Trinity study, once you have 25 times your annual expenses invested, you can withdraw 4% a year for 30 years with a 95% success rate.

It’s possible your dream life varies drastically from your life today. You can also multiply your current annual expenses by 25. This is the amount you’d need invested to retire with your current lifestyle.

By this point, you’ve explored two potential lifestyle goals and their costs. Write down these details about the financial goal you’ve landed on.

- Time (in years)

- Current value of investments (principal)

- Target future value of investments at end of time period

Estimate contributions

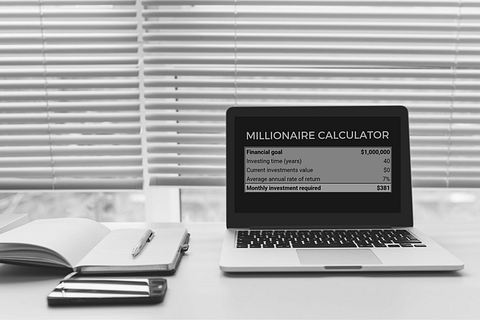

Once you have a clearly defined goal, you can use those targets to answer the question, how much should I invest? The calculation we are about to do is only an estimate.

That means even if you consistently invest the estimated amount from the calculation, you could still fall short of your goal.

Furthermore, the estimate may be an unrealistic investment amount for your current financial situation. That’s okay! Mine was too. We’ll address that in the next step.

To do this calculation, you will need a time/value of money calculator. If you’re a wizard in google sheets or Excel you can use the PMT function.

If not, you can grab a copy of my free google sheets investment calculator here. It has all the instructions you need to calculate your amount correctly.

Alternatively, you can use this free online calculator as well. If you decide to do the calculation yourself, I’m simplifying the steps to prevent miscalculations.

If you are using the Google Sheets calculator enter the following inputs:

- Annual target spend

- Investing time in years

- Current value of investments

The calculation produces your estimated monthly contribution to reach 25X your annual target spend, assuming a 7% average annual rate of return.

If you are using the PMT function or the online calculator, enter the following inputs:

- Your target future value (FV) = 25X your annual expenses

- Starting amount (PV) = Current value

- Number of periods (n) = Time in years

- Rate (R) = 7%, average annual rate of return

This calculates your estimated annual contribution amount. You can divide this by 12 to get a rough monthly estimate.

How did you feel when you looked at your payment amount? If this amount is achievable for you, then consider investing that amount monthly.

If this contribution amount wasn’t as realistic as you had hoped, we’ll address that in the next step.

Reconcile differences

Let’s determine what contribution amount is realistic for you. Then you can use this amount as your answer to how much should I invest. As your financial situation evolves, you can increase this amount when that becomes possible.

You can use the calculator to see how close that gets you to your goals. This time, you’ll enter the following inputs into your Google Sheets investment caclulator.- Monthly investment = realistic monthly investment contribution

- The planner will use the same time frame, current value, and average annual rate of return in the calculation above so it’s easy to compare.

The future value estimates the potential value of your investments at the end of the timeframe.

Alternatively, here’s an online future value calculator you can use. Enter the following inputs.

- Number of periods (n) = Time in years

- Starting amount (PV) = Current value

- Rate (R) = 7%, average annual rate of return

- Annual investment amount (PMT) = monthly investment amount x 12

Now we want to find a way to close the gap between your current landscape and ideal landscape. In other words, how can you increase your contribution amounts to reach your goals?

Most people may need to make adjustments to reach their goals. If you are in this situation too, you have several options:

- Re-evaluate your goal

- Increase investment contributions by re-allocating spending

- Increase investment contributions by earning more income

Re-evaluate your goal

Re-evaluating your goal will require in-depth self-reflection. You’ll want to explore what truly adds value to your life and what doesn’t. This may take some time to uncover any insights that could shift your goals.

For example, let’s say you currently spend $100,000 per year and want to do the same in retirement. Accordingly, you’d need ~$2.5 million invested to retire. Maybe after lots of introspection, you realize you only would need to spend $80,000 per year to live a dream life.

This would help you reach retirement faster in two ways.

- By lowering your spending from $100,000 to $80,000, you can invest the difference, an extra $20,000 per year! This will help you reach your goal faster, since you are investing more.

- Secondly, it also lowers your goal. You’d need ~$2 million invested to retire and withdraw $80,000 per year. The goal itself is easier to reach.

Adjusting your goals can significantly impact your answer to how much should I invest; however, it requires a high level of self-awareness. You must have a strong understanding of what truly adds the most value to your life.

Re-allocate spending

As more of a short-term solution, you could adjust your spending habits. This means you could spend less on the things that don’t add value to your life so you can invest more.

Adjusting your spending successfully will require some thoughtful planning. The Personal Finance Planner tracks your spending against your spending plan. This is a useful tool to evaluate your monthly spend against the joy it brings you.

Get started today by downloading your planner here.

Earn more income

So much personal finance advice tailored towards women is focused on spending less. Advice for men doesn’t do that!!! It’s because there’s a limit to how much you can cut.

At first lowering your spending can offer results quickly and painlessly, assuming you’re cutting things that don’t add value. After a certain point, you can’t cut an extra dollar without cutting something that adds a lot of value to your life.

So once your spending is under control, focus on earning more money instead. There’s a limit to how much you can reduce spending, but there’s no limit on how much you can earn.

Increasing your income is also a longer-term strategy. It may involve negotiating raises, accepting higher-paying jobs, or even starting your own side hustles.

If starting a business intrigues you, check out 7 ways to make money online here.

You don’t have to have all the answers today. Start by investing what you can and increase that contribution amount as you can.

Track your progress

This is the most important part of the process we discussed today. You MUST monitor your progress towards your goals for two reasons: it’s motivating and it prevents you from getting off track.

Choose a tool to track your investment contributions and subsequent net worth growth. Once I started tracking my progress with the Personal Finance Planner, I was able to double my net worth!

It’s helping other people reach their net worth goals and it can help you too.

Here’s how it helped one customer: “This tool organized all my financial information in one place. I finally have peace of mind now. I can quickly and clearly see what actions to take to reach my financial freedom. Love this!”

Download your planner today to see your progress towards your goals.

Conclusion

How much should I invest is a question everyone will have a unique answer to. It really depends on your current financial landscape and the financial goals you have.

After using the free investment calculator , you should have a good estimate of how much to invest each month to reach your financial goals.If your current financial situation doesn’t allow you to invest as much as you’d like, that’s okay! Health Self and Wealth is here to help you accomplish your financial goals.

Subscribe to receive email notifications for more resources that will help you build wealth.Thank yourself for taking the time to prioritize your financial well-being today. Your future self thanks you. 😉